Overview

Queensland’s local governments, also known as councils, play an important role in supporting the economic, social, and environmental wellbeing of communities. They are the first line of connection with our communities, providing Queenslanders with a wide range of services such as roads, water and waste, libraries, and parks.

Tabled 19 March 2026.

Report on a page

This report summarises the audit results of Queensland’s 77 local government entities (councils) and the entities they control.

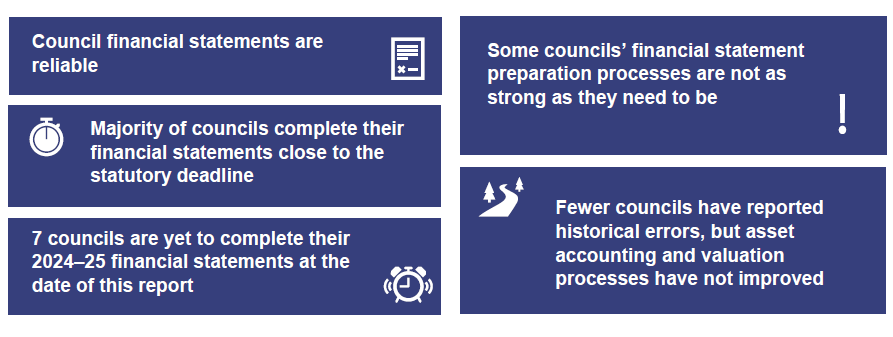

Financial statements for the sector are reliable

All councils had clean audit opinions, and their financial statements can be relied upon. This year, 63 councils (2023–24: 64 councils) had their financial statements completed by the statutory deadline of 31 October 2025.

Financial statements support the accountability and transparency of councils and allow for the comparison of Queensland councils with each other and other jurisdictions. They are comparable because all jurisdictions apply the same Australian accounting standards. Any change to the application of these standards needs to be carefully considered as it will reduce the comparability of council performance.

This year, councils improved the way they account for found and contributed assets, with fewer historical errors needing correction. Asset accounting and valuations still need improvement.

Access to skilled staff is a key driver for timely reporting

Councils’ financial statements are due for completion by the end of October each year. Around two-thirds of entities complete their financial statements just in time for that deadline or miss the deadline.

In preparing their financial statements, councils undertake checks and processes to ensure that the transactions and balances are complete and accurate. If a council does not have access to qualified and experienced staff, financial statements are more likely to contain errors and take longer to prepare and audit.

Continued focus needed to prevent fraud

In the past 2 years, 2 councils lost approximately $5 million as a result of inappropriately changing vendor bank account details. The sophistication of approaches by fraud perpetrators has increased, but the controls to protect vendor details should be effective. Independent validation of vendor and employee bank account changes is the critical control. All councils should regularly check their processes to protect these details.

There was multi-year former employee fraud within a controlled entity of a council.

Information systems and spending controls need attention

In 2024–25, there were 263 significant internal control deficiencies that were either new or unresolved – the highest number of high risk matters we have found in the sector in the last 5 financial years.

Controls relating to information systems, procurement, contract management, governance, and risk management need attention.

Changes in executive contract termination clauses

Standard terms and conditions are not used for executive contracts across the sector. There are significant differences in termination entitlements, which for chief executives vary from between 1 month and 12 months’ salary. Entitlements need to balance equity for the individual and appropriate use of public funds.

Each council should ensure that there is adequate oversight of contracts. The Department of Local Government, Water and Volunteers should provide guidance to the sector on chief executive contracts to ensure their adequacy and appropriateness.

1. Recommendations

Recommendations for councils

This year, we make one new recommendation for councils.

| Assess the termination clauses included in executive contracts to ensure they are appropriate (Chapter 5) |

|---|

We recommend councils assess the termination clauses included in their executive contracts to ensure they are appropriate for the public sector and required to attract, retain, and remunerate executives. Councils should ensure there is adequate oversight of terms and conditions in contracts. |

We have reported internal control deficiencies to individual entities during our audits.

By implementing our recommendations, councils will strengthen their internal controls for financial reporting and improve their financial sustainability.

Councils need to take further action on prior year recommendations

We encourage the councils to act on the recommendations from Local government 2024 (Report 13: 2024–25) that are not yet resolved. These are summarised in the following tables.

| Theme | Summary of recommendation | Local government report | Status of recommendation |

|---|---|---|---|

| Governance and internal control | Implement policies and procedures for determining the appropriateness and defensibility of ex-gratia payments [those made outside of contractual or legal requirements] including the transparency in such decision-making and the appropriateness of using non-disclosure agreements (Chapter 4) | Report 13: 2024–25 | Further action needs to be taken |

| Implement processes to ensure policies and procedures are regularly reviewed and kept up to date (Chapter 4) | Report 8: 2023–24 | Further action needs to be taken | |

| Annually review the registration status of employees undertaking engineering services (Chapter 4) | Report 8: 2023–24 | Further action needs to be taken | |

| Use our annual internal control assessment tool to help improve their overall control environment (Chapter 4) | Report 15: 2021–22 | Further action needs to be taken | |

| Improve risk management processes (Chapter 4) | Report 17: 2020–21 | Further action needs to be taken | |

| Establish and maintain an effective and efficient internal audit function (Chapter 4) | Report 13: 2019–20 | Further action needs to be taken | |

| Asset management and valuations | Review the asset consumption ratio – indicating how much of an asset has been used up – for water infrastructure assets and determine what action is required (Chapter 5) | Report 13: 2024–25 | Further action needs to be taken |

| Include councils’ planned spending on major capital projects in asset management plans (Chapter 5) | Report 15: 2021–22 | Further action needs to be taken | |

| Improve valuation and asset management practices (Chapter 3) | Report 17: 2020–21 | Further action needs to be taken | |

| Information systems | Strengthen the security of information systems (Chapter 4) | Report 17: 2020–21 | Further action needs to be taken |

| Conduct mandatory cyber security awareness training (Chapter 4) | Report 13: 2019–20 | Further action needs to be taken | |

| Procurement and contract management | Assess the maturity of their procurement and contract management processes using our procure-to-pay maturity model, and act on identified opportunities to strengthen their practices (Chapter 4) | Report 15: 2022–23 | Further action needs to be taken

|

| Enhance procurement and contract management practices (Chapter 4) | Report 17: 2020–21 | Further action needs to be taken | |

| Secure employee and supplier information (Chapter 4) | Report 13: 2019–20 | Further action needs to be taken | |

| Risk management | Assess climate risks and add them to the risk register (Chapter 4) | Report 13: 2024–25 | Further action needs to be taken |

We have included a full list of prior year recommendations and their status in Appendix E.

Recommendations for the Department of Local Government, Water and Volunteers

This year, we make the following new recommendation to the Department of Local Government, Water and Volunteers (the department).

| Develop guidance material on executive contracts for local governments (Chapter 5) |

|---|

| We recommend that the department develops guidance material to assist councils in developing contracts for executive employees. |

The department needs to take further action on prior year recommendations

The department has made some progress in addressing the recommendations we have made in our previous reports.

It has published a framework to help councils provide assurance over their internal controls, aimed at providing councils with guidance and structured approaches for implementing effective internal control systems. However, further action is still required on 2 recommendations, as summarised below.

| Theme | Summary of recommendation | Local government report | Status of recommendation |

|---|---|---|---|

| Financial reporting and capability within the sector | Introduce an internal controls assurance framework for councils (Chapter 4) Amend the Local Government Regulation 2012 to require the head of finance in each entity to confirm whether the financial controls used to prepare the annual financial statements are effective each year. | Report 8: 2023–24 | Not implemented |

| Financial sustainability | Amend the sustainability guideline to include an asset consumption ratio for each asset class (Chapter 5) | Report 13: 2024–25 | Not implemented |

We have included a full list of prior year recommendations and their status in Appendix E.

Reference to comments

In accordance with s.64 of the Auditor-General Act 2009, we provided a copy of this report to relevant entities. In reaching our conclusions, we considered their views and represented them to the extent we deemed relevant and warranted. Any formal responses from the entities are at Appendix A.

2. Entities in this report

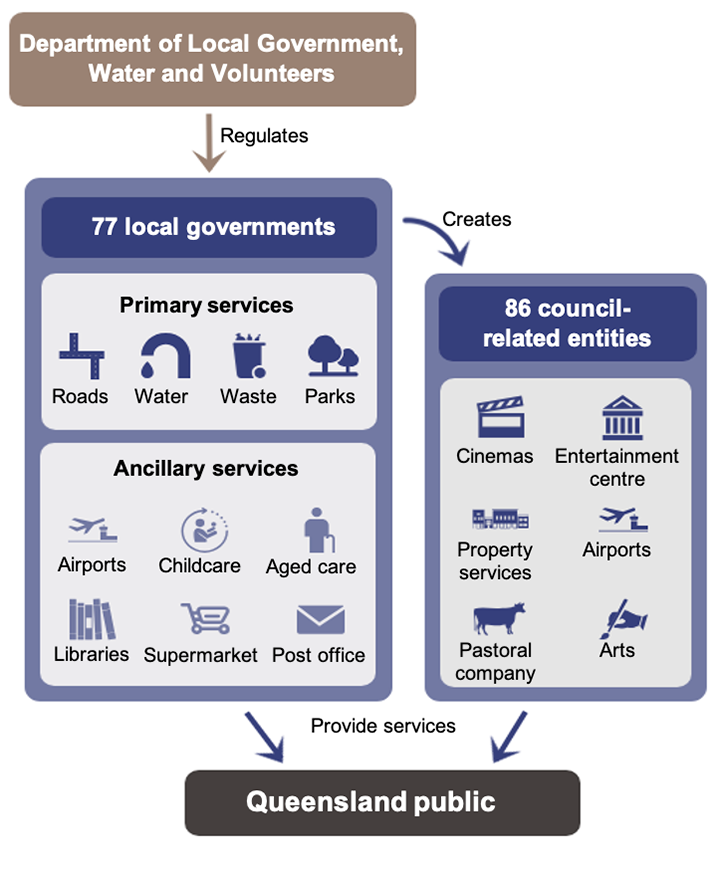

Queensland local governments (councils) are established under the Local Government Act 2009 or, in the case of the Brisbane City Council, under the City of Brisbane Act 2010.

These councils provide their communities with a range of primary and ancillary services, as shown in Figure 2A. They also establish council-related entities to separate commercial activities from the core regulatory and community service roles. These commercial activities can then be run like private businesses, while the councils continue to oversee and own them.

The Department of Local Government, Water and Volunteers regulates the sector and administers some of the funding programs.

Queensland Audit Office.

How entities are grouped in this report

The department, under its Financial Management (Sustainability) Guideline (2024) has grouped councils into tiers, as shown in Figure 2B, based on their remoteness and their population. This is for monitoring and reporting purposes. We refer to the councils by these tiers throughout our report for consistency and to perform more focused analysis. Figure 2B shows the tiers.

Tier 1 council | |||||

| Brisbane City Council | |||||

Tier 2 councils | |||||

| Cairns Regional Council | Logan City Council | Sunshine Coast Regional Council | |||

| Fraser Coast Regional Council | Mackay Regional Council | Toowoomba Regional Council | |||

| Gold Coast City Council | Moreton Bay City Council | Townsville City Council | |||

| Ipswich City Council | Redland City Council | ||||

Tier 3 councils | |||||

| Bundaberg Regional Council | Lockyer Valley Regional Council | Scenic Rim Regional Council | |||

| Gladstone Regional Council | Noosa Shire Council | ||||

| Gympie Regional Council | Rockhampton Regional Council | ||||

Tier 4 councils | |||||

| Cassowary Coast Regional Council | Mareeba Shire Council | Tablelands Regional Council | |||

| Central Highlands Regional Council | Somerset Regional Council | Western Downs Regional Council | |||

| Isaac Regional Council | South Burnett Regional Council | Whitsunday Regional Council | |||

| Livingstone Shire Council | Southern Downs Regional Council | ||||

Tier 5 councils | |||||

| Banana Shire Council | Douglas Shire Council | Maranoa Regional Council | |||

| Burdekin Shire Council | Goondiwindi Regional Council | Mount Isa City Council | |||

| Charters Towers Regional Council | Hinchinbrook Shire Council | North Burnett Regional Council | |||

Tier 6 councils | |||||

| Balonne Shire Council | Cook Shire Council | Torres Shire Council | |||

| Barcaldine Regional Council | Longreach Regional Council | ||||

| Cloncurry Shire Council | Murweh Shire Council | ||||

Tier 7 councils | |||||

| Barcoo Shire Council | Carpentaria Shire Council | McKinlay Shire Council | |||

| Blackall-Tambo Regional Council | Croydon Shire Council | Paroo Shire Council | |||

| Boulia Shire Council | Diamantina Shire Council | Quilpie Shire Council | |||

| Bulloo Shire Council | Etheridge Shire Council | Richmond Shire Council | |||

| Burke Shire Council | Flinders Shire Council | Winton Shire Council | |||

Tier 8 councils | |||||

| Aurukun Shire Council | Mapoon Aboriginal Shire Council | Torres Strait Island Regional Council | |||

| Cherbourg Aboriginal Shire Council | Mornington Shire Council | Woorabinda Aboriginal Shire Council | |||

| Doomadgee Aboriginal Shire Council | Napranum Aboriginal Shire Council | Wujal Wujal Aboriginal Shire Council | |||

| Hope Vale Aboriginal Shire Council | Northern Peninsula Area Regional Council | Yarrabah Aboriginal Shire Council | |||

| Kowanyama Aboriginal Shire Council | Palm Island Aboriginal Shire Council | ||||

| Lockhart River Aboriginal Shire Council | Pormpuraaw Aboriginal Shire Council | ||||

Compiled by the Queensland Audit Office, using the Department of Local Government, Water and Volunteers’ Financial Management (Sustainability) Guideline (2024).

3. Results of our audits

This chapter provides the results of our audits and the types of audit opinions given. It also provides areas of focus for councils for improving financial statement preparation and timeliness.

The main financial reporting challenge relates to asset accounting and valuation. This chapter provides more detail on the increased number of matters identified during our audits.

Chapter snapshot

Appendix E provides the full detail of all prior year recommendations we have made to councils and the department.

Audit opinion results

Audits of financial statements of councils and their controlled entities – 2024–25

All of the 2024–25 financial statements of the 70 completed councils (2023–24: 71 councils) were reliable and complied with relevant laws and standards. Of the 70 councils with finalised financial statements as of the date of this report, 63 were completed before the statutory deadline of 31 October.

Seven councils have not yet finalised their financial statements for 2024–25 and are outlined below:

- Boulia Shire Council

- Gympie Regional Council

- Mornington Shire Council

- Northern Peninsula Area Regional Council

- Palm Island Aboriginal Shire Council

- Woorabinda Aboriginal Shire Council (and prior years)

- Wujal Wujal Aboriginal Shire Council (and prior years).

They have all received approval from the Minister for Local Government and Water to extend their time frame to complete their financial statements.

Except for one audit opinion, the completed financial statements of the 64 council-related entities for 2024–25 were reliable and complied with relevant laws and standards. 14 council-related entities remain outstanding. The list of council-related entities that have not completed their financial statements for the 2024–25 year is included in Appendix F for controlled-entities, by-arrangement audits and jointly‑controlled entities, and Appendix G for exempt entities.

For Local Buy Trading Trust (controlled by the Local Government Association of Queensland Ltd), we issued a qualified opinion – we could not ensure that the revenue recorded in the financial statements was the total amount of revenue that it should have collected. We issued a qualified opinion for this entity last financial year for the same reason.

We included an emphasis of matter in the audit opinions for one council-related entity (2023–24: one council related entity) because it was reliant on financial support from its parent entity.

Not all council-related entities need to have their audits performed by the Auditor-General. Appendix G provides a full list of these entities.

Audits of financial statements of councils and their controlled entities – 2023–24 and 2022–23

Some councils and their controlled entities completed outstanding prior years’ financial statements in this financial year. Figures 3A and 3B show the councils and controlled entities that have completed their financial statements for 2022–23 and/or 2023–24, in the time since our last report.

Council | Financial year | Date audit opinion issued | Type of opinion issued |

|---|---|---|---|

| Northern Peninsula Area Regional Council | 2022–23 | 22.08.2025 | Unqualified |

| Palm Island Aboriginal Shire Council | 2022–23 | 24.04.2025 | Qualified |

| Diamantina Shire Council | 2023–24 | 11.04.2025 | Unqualified |

| Mornington Shire Council | 2023–24 | 29.08.2025 | Unqualified |

| Northern Peninsula Area Regional Council | 2023–24 | 19.12.2025 | Unqualified |

| Palm Island Aboriginal Shire Council | 2023–24 | 08.01.2026 | Qualified |

Queensland Audit Office.

We issued a modified audit opinion (qualified) on the 2022–23 financial statements of Palm Island Aboriginal Shire Council, as the council was unable to provide enough information about the completeness and accuracy of reported revenues for accommodation income, lease income, motel income, service charges, landing fees revenue, and staff salaries and wages expenses (and financial sustainability ratios based on these revenues and expenditure) to confirm that they were correctly reported.

We also issued a modified audit opinion (qualified) on the 2023–24 financial statements of Palm Island Aboriginal Shire Council, as the council was unable to provide enough information about the completeness and accuracy of reported revenues for accommodation income, lease income, motel income, service charges, and landing fees revenue (and financial sustainability ratios based on this revenue) to confirm that they were correctly reported.

Council controlled entities | Financial year | Date audit opinion issued | Type of opinion issued1 |

|---|---|---|---|

| Empire Theatres Foundation | 2022–23 | 27.01.2026 | Qualified |

| Empire Theatres Foundation | 2023–24 | 27.01.2026 | Unqualified with an emphasis of matter |

| Empire Theatres Pty Ltd | 2023–24 | 27.01.2026 | Qualified |

| TradeCoast Land Pty Ltd | 2023–24 | 05.09.2025 | Unqualified with an emphasis of matter |

| Ipswich Arts Foundation Trust | 2023–24 | 19.05.2025 | Unqualified |

| Major Brisbane Festivals Pty Ltd | 2023–24 | 12.05.2025 | Unqualified |

| SEQ Regional Recreational Facilities Pty Ltd | 2023–24 | 05.08.2025 | Unqualified |

| Townsville Breakwater Entertainment Centre Joint Venture | 2023–24 | 06.05.2025 | Unqualified with an emphasis of matter |

Note: 1 Refer to Appendix F for further details on the various emphases of matter.

Queensland Audit Office.

We issued a qualified opinion for Empire Theatres Foundation’s 2022–23 financial statements and Empire Theatres Pty Ltd's 2023–24 financial statements, due to alleged fraud.

Unfinalised audits of financial statements of councils and their controlled entities – 2021–22, 2022–23, and 2023–24

Figures 3C and 3D show the councils and controlled entities that have not yet completed their financial statements for prior years. These councils have all received approval from the Minister for Local Government and Water to extend their time frame.

Council | Financial year | Status | Ministerial extension issued to date1 |

|---|---|---|---|

| Woorabinda Aboriginal Shire Council | 2021–22 | Not complete | 02.03.2026 |

| Woorabinda Aboriginal Shire Council | 2022–23 | Not complete | 29.05.2026 |

| Woorabinda Aboriginal Shire Council | 2023–24 | Not complete | 29.05.2026 |

| Wujal Wujal Aboriginal Shire Council | 2023–24 | Not complete | 31.03.2026 |

Note: 1 Ministerial extensions may only be obtained for councils (not local government-related entities).

Queensland Audit Office.

Council | Financial year | Status |

|---|---|---|

| Woorabinda Pastoral Company Pty Ltd | 2021–22 | Not complete |

| Woorabinda Pastoral Company Pty Ltd | 2022–23 | Not complete |

| Woorabinda Pastoral Company Pty Ltd | 2023–24 | Not complete |

| North Rail Yard Developments Pty Ltd | 2023–24 | Not complete |

Note: * Ministerial extensions are not required for controlled entities that have not completed their financial statements.

Queensland Audit Office.

We express an unmodified opinion when financial statements are prepared in accordance with the relevant legislative requirements and Australian accounting standards.

We include an emphasis of matter to highlight an issue of which the auditor believes the users of the financial statements need to be aware. The inclusion of an emphasis of matter paragraph does not change the audit opinion.

We express a modified opinion when financial statements do not comply with the relevant legislative requirements and Australian accounting standards and, as a result, are not accurate and reliable.

There are 3 types of modified opinions: qualified, adverse, and disclaimer.

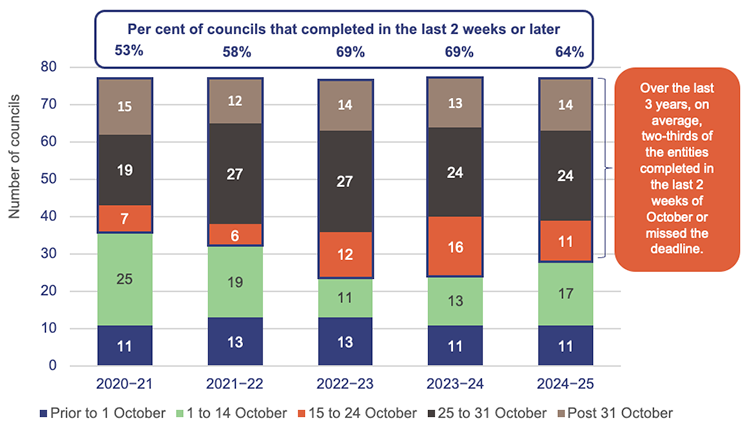

Focus areas for improving the timeliness of financial reporting

Councils in Queensland have until 31 October each year to have their financial statements prepared, approved, and audited. State government entities complete their financial reports by 31 August each year.

Reporting by 31 October ensures that the community, councillors, and management have timely access to reliable financial information. Allowing sufficient time to prepare and audit financial statements improves their quality and supports their delivery by the end of October.

Around two-thirds of councils complete their financial statements very close to the legislative deadline or miss the deadline. This can add pressure to the finance teams, and preparation and review processes. We find that late processes often increase the risk of error. It also compresses the time available for councils, their audit committees, and auditors to consider matters that require significant attention.

In the last 3 years (2022–23 to 2024–25), more councils have either completed their financial statements late in October or have not met their statutory deadline.

This is particularly challenging for several rural and remote councils in tiers 7 and 8, largely due to their inability to access skilled finance staff. Qualified and experienced finance staff are in demand, and many Queensland councils have found it difficult to recruit and retain them. In Chapter 5 of this report, we suggest ways in which councils could work collaboratively to boost their capability.

Figure 3E shows the timeliness of financial reporting across the sector.

Queensland Audit Office.

Some of the milestones were not met because agreed timetables for the preparation of statements and supporting working papers were not met. These timetables are agreed at the beginning of the preparation and audit processes.

Financial reporting processes can be improved

Financial reporting processes are the end-to-end activities that councils use to record, reconcile, review, and report financial information. These processes help make sure financial information is complete, accurate, and reported on time for monthly reporting and the annual financial statements. Oversight of financial reporting processes and strong internal controls helps ensure issues are identified early, addressed promptly, and do not affect the quality of the financial statements.

This year, we reported 72 weaknesses (2023–24: 94 weaknesses) related to councils’ financial reporting processes. Although this is an improvement, as of 30 June 2025, all 72 weaknesses (2023–24: 78 weaknesses) are still unresolved. Of these, 64 weaknesses have not been resolved for more than 12 months.

Section snapshot 3.1 – all weaknesses in financial reporting processes in 2024–25

Developing mature financial statement preparation processes

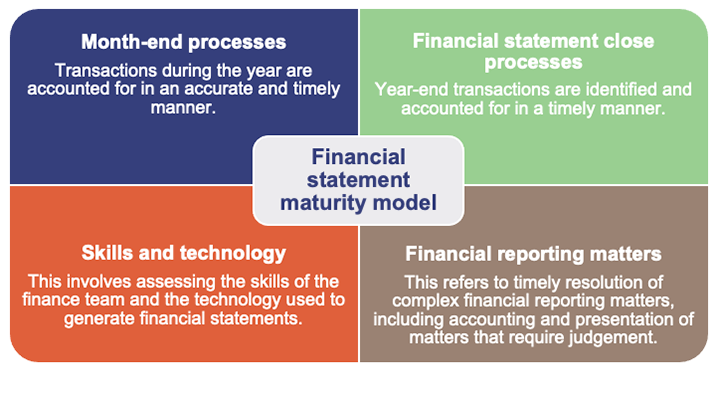

Timely financial reporting is supported by mature financial statement preparation processes. These include month-end processes, year-end processes, access to skills and technology, and the timely identification and response to financial reporting matters. Many of these processes are undertaken throughout the year, which eases year-end pressures.

To assist public sector entities in Queensland strengthen their financial statement preparation processes, we developed a financial statement maturity model. It is available on our website at: www.qao.qld.gov.au/reports-resources/better-practice/financial-statement-preparation-maturity-model-self-assessment. This model assesses financial statement maturity processes across the following 4 components.

Queensland Audit Office.

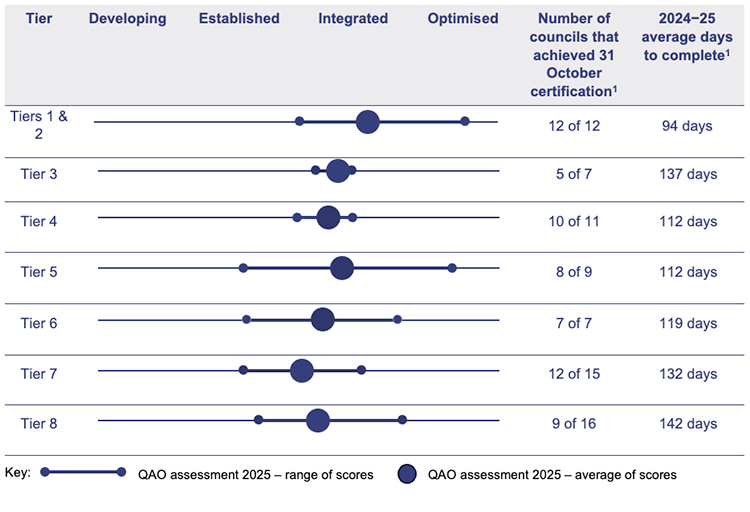

This year, we assessed councils’ financial statement maturity levels using this tool. Figure 3G aggregates the maturity levels for councils in each tier. While there is a wide range of maturity levels, typically the lower the maturity, the fewer the councils meeting their statutory deadlines and the longer the average days to complete financial statements.

Notes: This graph shows the minimum and maximum score for each council within the Tier, and the average of all scores.

1 Average number of days each tier has taken to have its audit opinions certified from 30 June 2025 per tier (number of days between 30 June and 31 October is 123). For councils that have not signed their financial statements at the date of this report, we have used 31 January 2026 as a proxy for their completion date.

Compiled by the Queensland Audit Office, based on information collected from QAO assessments (2024–25), using our financial statement preparation maturity model self-assessment tool.

We show the maturity levels and the number of days to complete the financial statements for each council in Appendix J.

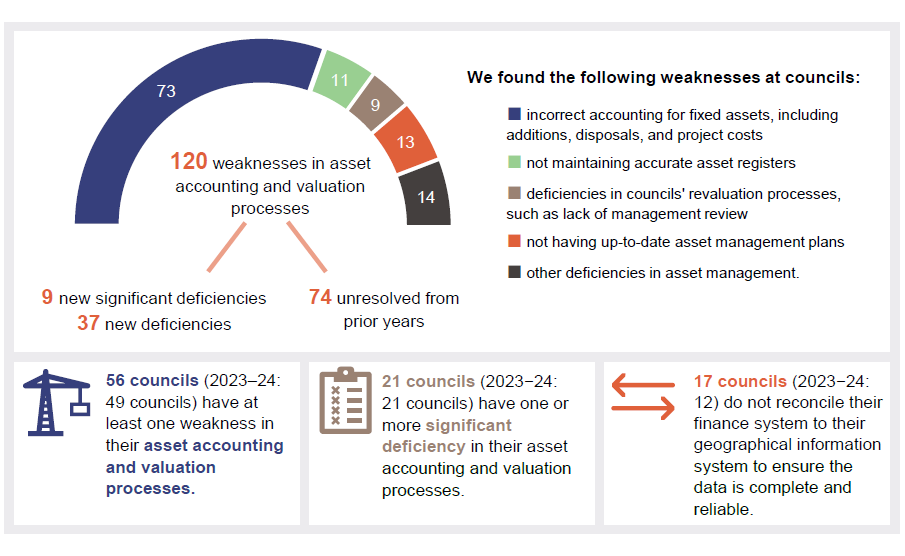

Asset accounting and valuation processes need more focus

As of 30 June 2025, the sector managed $148 billion of infrastructure assets (2023–24: $142 billion). These include roads, bridges, and water assets that are used to provide services to their communities. Councils have improved their record keeping relating to contributed assets, resulting in fewer historical (prior period) errors identified this year.

Accounting for and valuing assets, combined with good record keeping, continue to need improvement and make up a number of significant deficiencies we report to councils. Up-to-date and reliable asset information supports financially sustainable council decision making, including where to spend money on repairs and maintenance as well as the upgrade or replacement of assets. It can also help inform procurement planning and supply chain management.

We categorise any required improvements we identify as either a significant deficiency or deficiency. A significant deficiency is of higher risk and requires immediate attention by a council.

Section snapshot 3.2 – all asset accounting and valuation weaknesses in 2024–25

Asset accounting and asset valuation processes need improvement

We continue to identify weaknesses in asset accounting and valuation. This year, we identified 46 new weaknesses (2023–24: 39 weaknesses) in these processes. We noted:

| errors in or changes to the asset valuation identified in the audit process |

| untimely reporting by valuers, in some instances because councils did not engage early with the valuers |

| lack of oversight by management of the asset valuation process, resulting in delays in finalising the valuations. |

Councils’ assets are the largest amount in their financial statements. Valuing these assets is complex and requires significant estimates and judgements. Sufficient time needs to be allocated – both by councils and auditors – for this process to ensure that the value of the assets reported in council financial statements are correct.

Councils that have good asset valuation processes ensure they have their asset valuation completed by 30 June each year. This gives them enough time to properly oversee the process and consider the results of the valuations, which helps with timely preparation of financial statements.

Preparing position papers for asset valuations

Councils can either prepare their valuations internally or engage an external valuer to support the process. Analysing the results of either process ensures that the determined values are appropriate, and based on the current condition of the assets and the way they are used and maintained.

Those responsible for oversighting the financial reporting process should challenge the fair values and useful lives (how long the assets would last before they need to be replaced) assigned to assets. This would help avoid asset values being overstated and higher depreciation charges.

We have previously issued guidance to entities on preparing good documentation – referred to as ‘position papers’ – for accounting matters and valuation. Our fact sheet includes guidance on the content to be included in position papers, and some example papers. It is available on our website at: www.qao.qld.gov.au/reports-resources/fact-sheets/preparing-position-papers-accounting-matters-valuation.

Fewer prior period errors relating to found assets

Fewer councils identified ‘found’ assets in the 2024–25 financial year. Five councils (2023–24: 11 councils) accounted for a combined $136 million (2023−24: $255 million) of found and contributed (donated) assets, which is a reduction of 46 per cent compared to last year.

Councils are strengthening how they identify and account for assets that are donated to them – by developers or through other sources, such as other levels of government – and for found assets (these are the assets that councils have owned but not previously accounted for in their records).

One of the reasons that councils still identify found assets is because the information recorded in their financial systems and geographical information systems – which are used to capture, store, and manage detailed components of assets, including their geographical location – do not agree with each other.

Regular reconciliation of the financial systems to the geographical information system would help councils ensure that the records of assets in their financial statements are complete and accurate.

We encourage councils to continue improving their process for identifying and accounting for assets in a timely manner.

4. Internal controls at councils

This chapter reports on the effectiveness of the internal controls of the local government sector. It also provides areas of focus for entities to improve their internal controls.

Internal controls are the people, systems, and processes that ensure an entity can achieve its objectives, prepare reliable financial reports, and comply with applicable laws. Features of an effective internal control environment include:

- a strong governance framework that promotes accountability and supports strategic and operational objectives

- secure information systems that maintain data integrity

- robust policies and procedures, including appropriate financial delegations

- regular management monitoring and internal audit reviews.

Where we identify weaknesses in the internal controls, we categorise them as either deficiencies (those of lower risk that can be corrected over time) or significant deficiencies (those of higher risk that require immediate action by management). We report any weaknesses in the design or operation of those internal controls to management for their action.

Chapter snapshot

Appendix E provides the full details of all prior year recommendations made to councils and the department.

Types of internal control deficiencies across the sector

We assess whether the systems and processes (internal controls) used by entities to prepare financial statements are reliable.

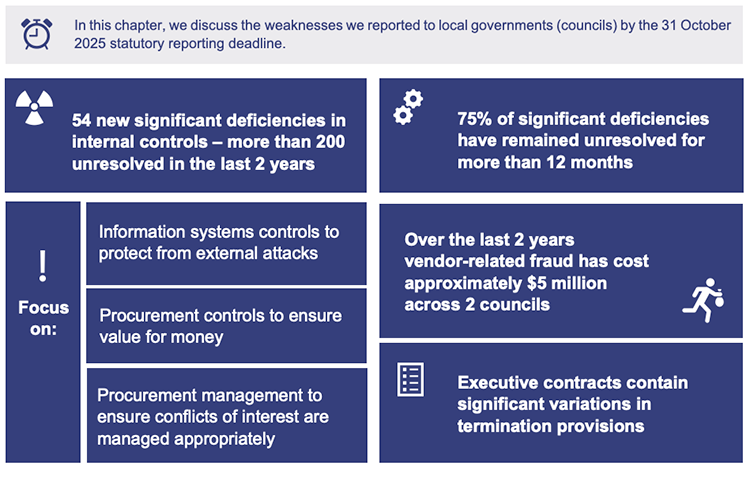

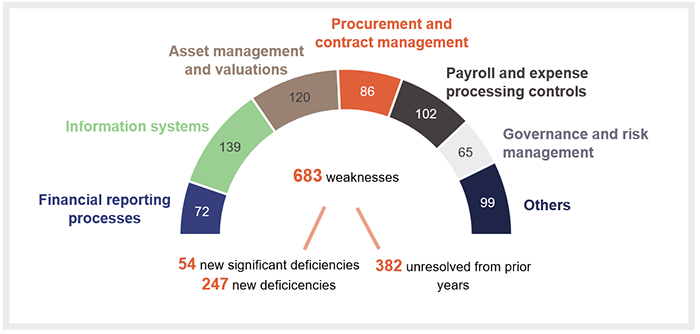

This year, we have reported 301 new weaknesses, including 54 new significant deficiencies across 31 councils (2023–24: 242 new weaknesses, including 52 new significant deficiencies). Figure 4A shows the type of weaknesses we have identified across councils in our audits this year.

Compiled by the Queensland Audit Office.

All of the common internal control weaknesses shown in Figure 4A are covered in this report. We discussed internal control deficiencies related to the financial statement preparation process, including financial reporting processes and asset management and valuations in Chapter 3.

In this chapter, we cover the other common internal control weaknesses shown in Figure 4A above. We also give an update on internal control actions from prior years.

More action is needed to resolve overdue internal control weaknesses

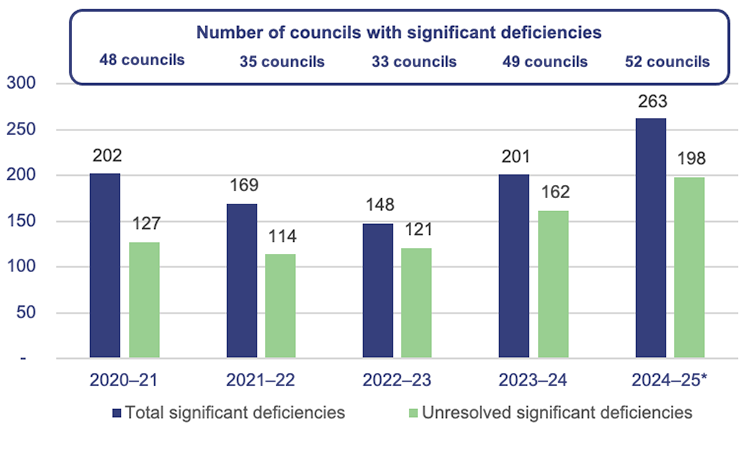

The number of weaknesses unresolved from prior years as of 30 June 2025 had increased to 382 (2023–24: 356), with two-thirds of councils having unresolved significant deficiencies.

We have reported more than 200 significant deficiencies that were either new or unresolved from previous years. Of these, 75 per cent (2023–24: 81 per cent) have remained unresolved for more than 12 months. We classify a deficiency as significant when we consider that it needs immediate attention due to the risks associated with the matter.

Councillors, chief executives, and audit committees must ensure they are informed of the reported matters, risks to council, and action plans that are in place. Active oversight and management are necessary to resolve the deficiencies.

Councils without audit committees and/or internal audit functions have more outstanding actions relating to internal control deficiencies. We discuss this later in the chapter.

Figure 4B shows the total significant deficiencies and unresolved significant deficiencies across the sector for the last 5 financial years.

Note: * Number of significant deficiencies reported for 2024–25 includes significant deficiencies from 2020–21, 2021–22, 2022–23, and 2023–24 for councils that completed their financial statements since we tabled Local government 2024 (Report 13: 2024–25) in April 2025.

Queensland Audit Office.

Common internal control deficiencies that are not resolved by councils

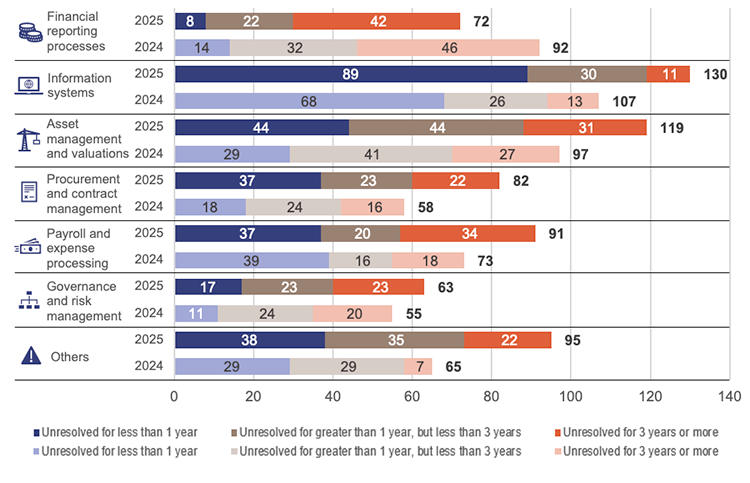

As of 30 June 2025, 28 per cent (2023–24: 23 per cent) of councils’ unresolved deficiencies have been outstanding for more than 3 years, showing that they are not addressing issues in a timely way. In Figure 4C, we show the sector’s internal control deficiencies grouped by theme and how long they have remained unresolved.

Note: Weaknesses related to the financial statement preparation process, including financial reporting processes and asset management and valuations, are discussed in Chapter 3.

Queensland Audit Office.

Themes of common internal controls weaknesses

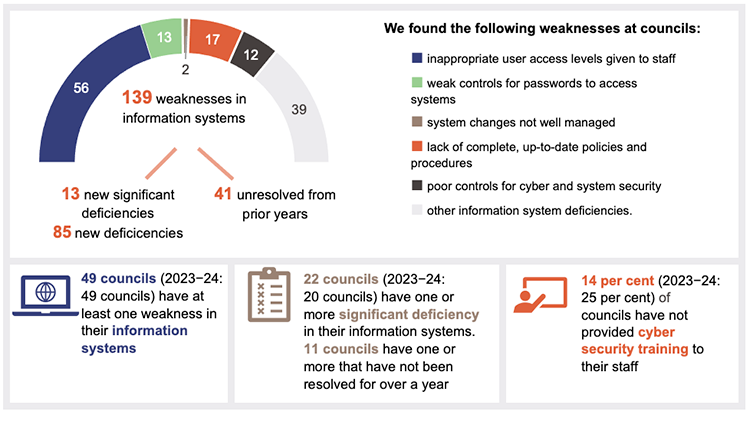

Most information system weaknesses relate to inappropriate access to systems

Section snapshot 4.1 – all weaknesses in information system controls in 2024–25

Source: Queensland Audit Office.

Information systems are an integral part of a council’s day-to-day operations. They store financial and non-financial data for the council, its employees, vendors (suppliers), and rate payers.

As part of our audit, we review each council’s information systems control and recommend actions to strengthen their control environment. These actions, if put in place, do not guarantee that councils are immune to cyber threats, but they provide baseline protection.

This year we identified 98 new weaknesses across 49 councils (2023–24: 77 new weaknesses across 49 councils).

Many of these weaknesses relate to councils not assigning the right level of access that their staff need to undertake their day-to-day responsibilities. When entities do not provide the appropriate access levels, they expose their data to unauthorised access and potentially to the risk of cyber attack.

Cyber threats have been on the rise and are becoming more sophisticated. Over the last few years, we have tabled a number of reports that can help councils identify, manage, and respond to cyber threats. Figure 4D highlights the key takeaways from these.

Report | Take away for councils |

|---|---|

| Managing cyber security risks (Report 3: 2019–20) | This report includes the fundamentals of how entities can manage their cyber security risks. The report refers to the 'Essential Eight' mitigation strategies published by the Australian Cyber Security Centre. |

| Responding to and recovering from cyber attacks (Report 12: 2023–24) | This report discusses how entities should respond to and recover from a cyber security incident. This report also includes the following better practice guides:

Both guides are available on our website at: www.qao.qld.gov.au/reportsresources/better-practice |

Queensland Audit Office.

Cyber risk also emanates from third parties that provide services to councils – typically those that are managing councils’ information technology systems. Councils need to have sound processes to manage these risks.

Our Forward work plan 2025–28 includes a future audit to assess in detail how effectively public sector entities manage third-party cyber security risks.

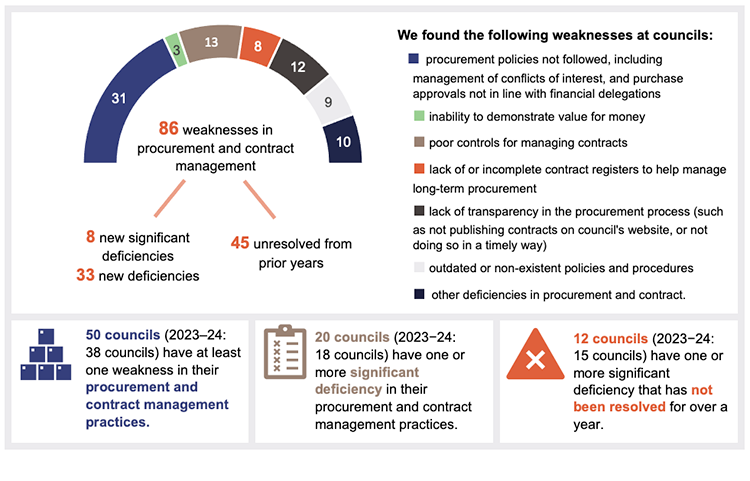

Procurement and contract management controls need more attention to ensure councils achieve value for money

Section snapshot 4.2 – all procurement and contract management weaknesses in 2024–25

Source: Queensland Audit Office.

The sector spends approximately $11.7 billion on average per year on operational and capital (major construction or replacement of assets) purchases.

As of 30 June 2025, over 60 per cent of the sector had weaknesses in procurement and contract management processes. We identified 41 new weaknesses in the 2024–25 financial year (2023–24: 21 new weaknesses).

Strong processes, including oversight, are needed to help:

- the decision-making process on what to procure, who to procure from, and whether what is offered provides value for money

- managing potential, actual, or perceived conflicts of interest throughout this process to support transparency and accountability

- ensure compliance with council’s own policies or the Local Government Regulation 2012.

The processes should also assess the performance of a council's vendors to ensure they have met requirements under their contractual arrangements.

To assist councils improve their procurement and contract management practices, in 2023 we developed a procure-to-pay model for local governments. It is available on our website at: www.qao.qld.gov.au/reports-resources/better-practice/local-government-procure-pay-model. This model contains a series of questions, grouped by 5 key components of internal control.

Managing conflicts of interest improves accountability and trust

Identifying and managing councillor and employee conflicts of interests ensures that the public can trust that the interests of council come first. We found significant deficiencies in some council processes for managing conflicts of interest.

Conflicts of interest generally arise when private interests, such as financial activities and relationships, impact, or appear to impact, judgements while performing council work. These can take many forms, including:

- obtaining direct or indirect financial benefits, or avoiding a loss

- sharing information with member organisations

- family member or close relationship benefits.

There should be appropriate processes to ensure that conflicts of interest are declared and managed, particularly during key decision making, procurement activity, grant allocations, and appointment and management of staff. Properly managing conflicts builds trust and manages the risk of any perceived wrongdoing.

| Opportunities for councils – managing conflict of interest effectively Systems for managing conflicts of interest should comprise policies, procedures, and tools that link together:

|

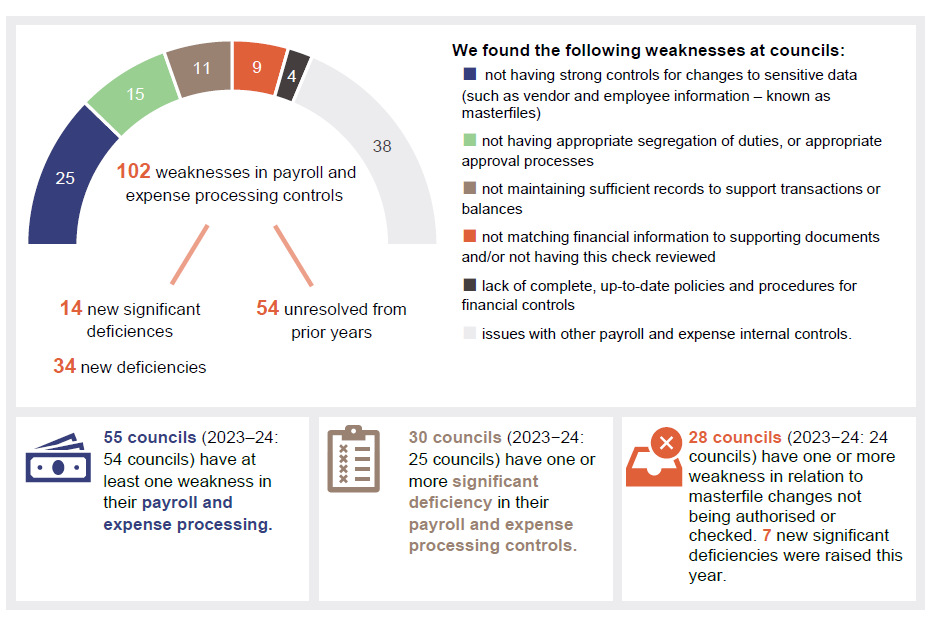

Weaknesses in payroll and expense processing controls leave councils vulnerable to fraud and error

Section snapshot 4.3 – all payroll and expense processing control weaknesses in 2024–25

Payroll and expense processing controls ensure councils pay the right people the right amounts on time and record those costs accurately.

This year, we reported 48 new weaknesses (2023–24: 54 weaknesses) in the controls councils have in place over their payroll and expenses processing activities. Included in this are 7 new significant deficiencies (2023–24: 13 new significant deficiencies) in relation to insufficient independent reviews being performed over supplier and/or employee masterfile changes.

These reviews reduce the risk of errors, fraud, and incorrect payments by making sure balances are checked against supporting documents and changes to employee or supplier details are properly reviewed.

Controls over changes to masterfile data protect against fraud

Vendor fraud typically involves a fraudster posing as a legitimate vendor and requesting the entity to change the bank details of the legitimate vendor to those of the fraudster. When the legitimate invoices are received and processed, the payment goes to the fraudster’s bank account. The approach by those perpetrating these frauds has become more sophisticated, highlighting the need to independently verify all changes to vendor details.

The Queensland public sector has been impacted by these vendor frauds for almost a decade. In the 2024–25 financial year, another council was impacted by an instance of supplier fraud. Two councils have lost a combined $5 million over the last 2 financial years to vendor fraud, with only a portion of this being recovered.

In both instances, internal controls did not operate in the way they were designed to, resulting in losses of public monies and reputational damage to these councils.

Multiple recommendations have been made to councils to review their internal controls relating to vendor and employee masterfile details. In the box below, we have provided some opportunities for councils to consider in strengthening the internal controls when changes are made to vendor master file.

|

| Opportunities for councils – strengthen internal control over changes to masterfiles and reinforce the importance of good controls to the staff To help prevent successful fraudulent attempts, and to improve internal controls, all entities must take the following actions:

|

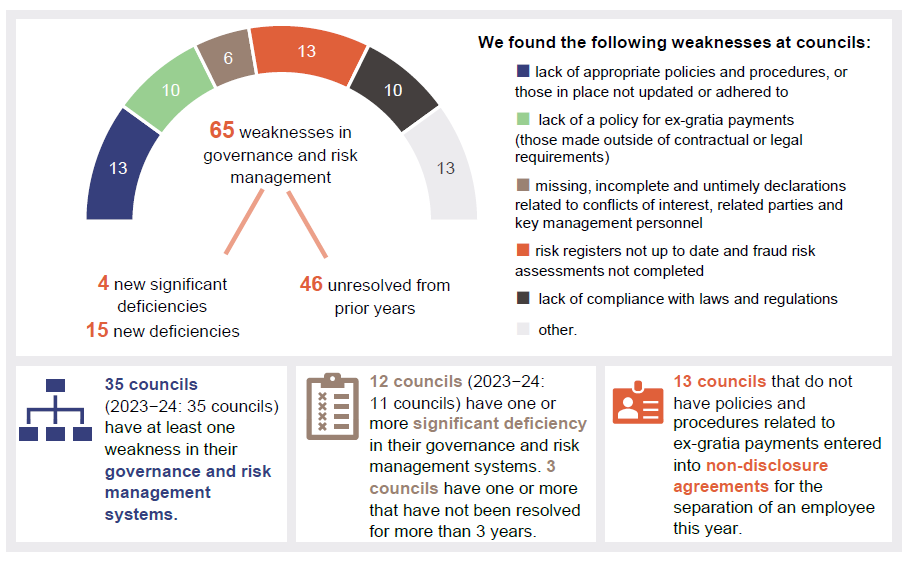

Governance and risk management processes need attention

Section snapshot 4.4 – all governance and risk management weaknesses in 2024–25

Governance sets the direction, expectations, and oversight of councils, while risk management helps identify and manage the risks that could stop them from achieving their objectives.

This year, we identified 19 new control weaknesses (2023–24: 11 weaknesses) in governance and risk management practices at councils. Councils have not been resolving their governance and risk management-related issues from previous years.

Insufficient and outdated policies and procedures can undermine councils’ performance

Policies and procedures are important elements of councils’ governance and risk management frameworks, as they help shape their culture and internal control environment. Having good policies and procedures promotes consistent practices.

This year, we reported 30 weaknesses (2023–24: 38 weaknesses) in relation to outdated policies and procedures. While there has been some improvement, councils need to take further action to strengthen them.

Varied termination clauses in executive contracts

Executive leaders (including chief executive officers) are usually employed under fixed term contracts. These contain the terms and conditions of employment, including what payments executives are entitled to receive if their employment is terminated. There are no standard terms for these executive contracts, and each council determines their own contractual requirements, sometimes without seeking any expert advice.

The common difference between contracts relates to termination clauses, which for chief executives vary from between 1–12 months of their overall remuneration – most entitlements being for 6 months remuneration. With the level of turnover in council chief executives reaching 39 per cent following the March 2024 elections, the costs to the sector can be substantial. 24 councils determined the termination clauses and the conditions without any consultation with an expert.

In the Queensland state sector, senior executives are employed under the Public Sector Act 2022 and have a standard employment contract that limits any separation payments up to 6 months depending on the remaining duration of the contract at termination or 12 weeks on mutual agreement.

In New South Wales, the Office of the Local Government has mandated the use of standard contracts of employment when executives are employed by local governments in the state. This ensures consistency and certainty in employment relationships and reflects community expectations by providing greater transparency and accountability.

The Department of Local Government, Water and Volunteers (the department) has a role in developing similar guidance for the local government sector, to promote greater consistency in the terms and conditions for chief executive officer contracts.

Recommendation to councils Assess the termination clauses included in executive contracts to ensure they are appropriate.

|

Recommendation to the department Develop guidance material on executive contracts for local governments We recommend that the department develops guidance material to assist councils in the development of their executive contracts. |

Most councils do not have a policy on ex-gratia payments

In Local government 2024 (Report 13: 2024−25), we reported that councils collectively paid $6.4 million in termination payments to key management personnel. Included in these termination payments were amounts totalling to $1.4 million paid over and above what these executives were entitled to under their employment contracts. These amounts are referred to as ‘ex-gratia’ payments.

Last year, we recommended councils implement policies and procedures to establish an approved framework within which they could make decisions around ex-gratia payments. Such a policy would guide when such payments are appropriate, a basis on which to determine the amount to be paid, and clarify who can approve such payments.

As of 30 June 2025, only 20 councils had developed a policy on ex-gratia payments.

Councils that had made ex-gratia payments in the 2023–24 financial year had done so using non‑disclosure agreements (NDAs). While there are situations where NDAs might be necessary to protect sensitive information or privacy, it is important to ensure that they are used only in appropriate circumstances and that there is oversight. There is an increased risk that NDAs may be used to conceal suspected wrongdoing or make large payments that are more difficult to justify.

Risks arise when entities do not segregate duties

Segregation of duties ensures that no single person has control over all aspects of a financial transaction. This helps protect an organisation from fraud and error.

This can be challenging for smaller entities, as typically there is only one staff member in their finance team. In these circumstances, this oversight could come from those that are responsible for managing the business, such as the chief executive officer, or from those responsible for setting the strategic direction of the entity such as board of directors (for council-controlled entities) or by other senior employees in the case of small councils.

This year, an instance of fraud was reported at one council-controlled entity. The council has requested the controlled entities to improve payment and segregation controls. The council is continuing to undertake reviews to implement financial and governance improvements.

Councils can improve financial controls by implementing an internal controls assurance framework

In Local Government 2023 (Report 8: 2023–24) we recommended the Department of Local Government, Water and Volunteers (the department) develop a template that councils could use to annually validate the effectiveness of their internal controls. This provides the chief executive officers and mayors – who sign the financial statements – with assurance that the amounts in the financial statements are correct.

In May 2025, the department published an internal controls assurance framework (the assurance framework) for councils. The framework provides councils with guidance and structured approaches for the implementation of effective internal control systems that align with best practice and support their sustainability.

This year, only 7 councils completed an assurance framework and attested that the financial controls they used to prepare the financial statements were effective.

Using a framework would provide councils with an opportunity to assess, implement, and improve internal controls.

Councils that have their own framework should compare it to the one issued by the department and consider any changes they need to make to their existing frameworks. Other councils can consider scaling the department’s framework to suit the size and nature of their organisation.

Below, we show the benefits that preparing an assurance statement will bring about to councils’ financial statement processes.

|

| Opportunities for councils – preparing an assurance statement to validate the effectiveness of internal controls The assurance process provides several benefits for councils, chief executive officers, and mayors. It:

|

Effective audit committee and internal audit functions enhance the governance framework in councils

What do audit committees do?

An effective audit committee supports the chief executive and council by providing oversight of financial reporting, internal control systems, risk management systems, and internal audit.

Audit committees can often be a cost-effective independent source of advice on aspects of council operations that are required each year – preparing annual financial statements, having those financial statements audited, and running an internal audit function. In addition, audit committees can help improve accountability by challenging councils on their financial and risk management processes and the timely resolution of internal control deficiencies.

In the case study in Figure 4E, we provide an example how an audit committee at a regional council works with the council’s internal auditors and management.

| Effective monitoring and reporting to an audit committee can help resolve outstanding audit recommendations in a timely manner |

|---|

At each meeting, the audit committee of a regional council receives a comprehensive status report showing the number of audit recommendations that are unresolved. This includes recommendations made by the internal auditors on operational matters as well as those raised in the external financial audit. The report breaks this information down by risk rating and compares it with previous periods. This allows the audit committee to quickly identify movements, recurring issues, and areas requiring attention. Significant deficiencies are reported separately given their risk to council. A simple traffic-light system is used to highlight the level of effort required to resolve each deficiency, making it easy to see where management’s attention is needed. Using clear and up-to-date information, the audit committee can challenge internal audit and management on the progress. Where appropriate, the committee helps identify practical solutions to remove obstacles. By using consistent reporting, comparing progress over time, and focusing on high-risk items, the audit committee maintains strong oversight and ensures emerging risks and delays are identified early and addressed promptly. |

Queensland Audit Office.

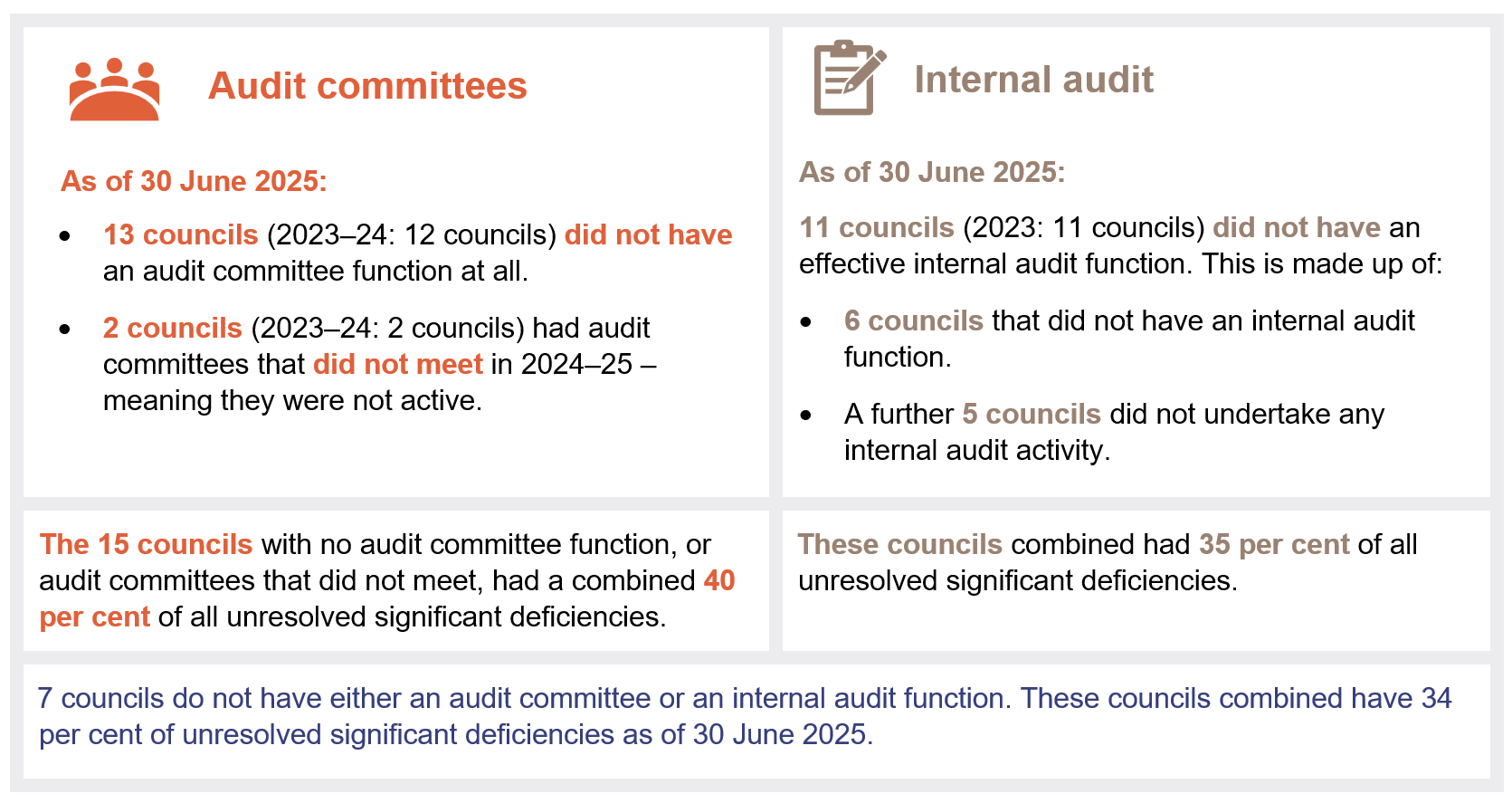

Some councils do not have an audit committee function

At 30 June 2025, 13 councils (2023–24: 12 councils) do not have an audit committee.

In our reports of local government financial audits over the years, we have recommended that all local governments establish audit committees to help improve their oversight of governance and financial responsibilities.

What does internal audit do?

An internal audit function assesses operations and reviews governance, risk management, and control processes. Internal auditors evaluate risks and can assist in establishing strong fraud prevention measures by assessing the strengths and weaknesses of controls.

Not all councils have internal audit, and some use this function to provide support to the finance function

At 30 June 2025, 6 councils (2023–24: 6 councils) do not have an internal audit function.

As of 30 June 2025, 11 of the 71 councils that had an internal audit function use their internal auditors to provide support for their finance function. They post transactions in their councils’ accounting systems, prepare monthly management reports, and help with year-end process, which includes preparing position papers and financial statements. Due to the extent of their involvement in finance related functions, they are often unable to perform their internal audit role effectively as there is limited remaining time or they are unable to provide an objective view of finance processes.

Councils that do not have audit committees and/or internal audit functions have more unresolved significant deficiencies

Figure 4F shows that councils that do not have an audit committee and/or an internal audit function have a large number of unresolved significant deficiencies.

Queensland Audit Office.

Update on the internal controls of entities that missed the deadline for last year’s report

At the time we compiled Local government 2024 (Report 13: 2024−25), 13 councils had not completed their financial statements by the legislative deadline.

Since then, 9 of these 13 councils have completed the financial statements. Our audit of these councils identified 19 new significant deficiencies and 16 new deficiencies in their internal control processes.

The 19 new significant deficiencies are as follows:

Information systems |

Procurement and contract management |

Governance and risk management |

Other |

|---|---|---|---|

| 6 significant deficiencies covering user access for systems, system changes, and reporting. | 5 significant deficiencies relating to councils not following procurement and contract management policies and recordkeeping. | 3 significant deficiencies over governance and compliance with laws and regulations. | 5 significant deficiencies covering month-end processes, not appropriately checking changes to vendors’ bank account details, or not appropriately billing and reporting revenue. |

5. Financial performance of councils

This chapter analyses the financial performance of local governments (councils), with emphasis on their financial sustainability. This is measured against the Financial Management (Sustainability) Guideline (2024), issued by the Department of Local Government, Water and Volunteers (the department).

Chapter snapshot

Financial performance of councils

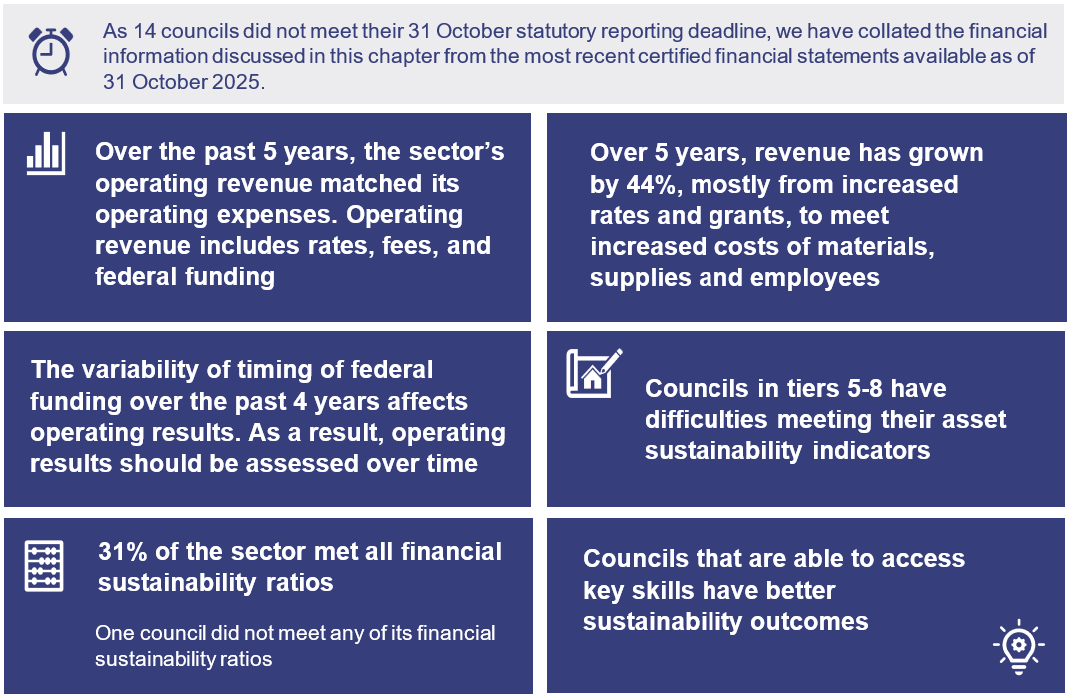

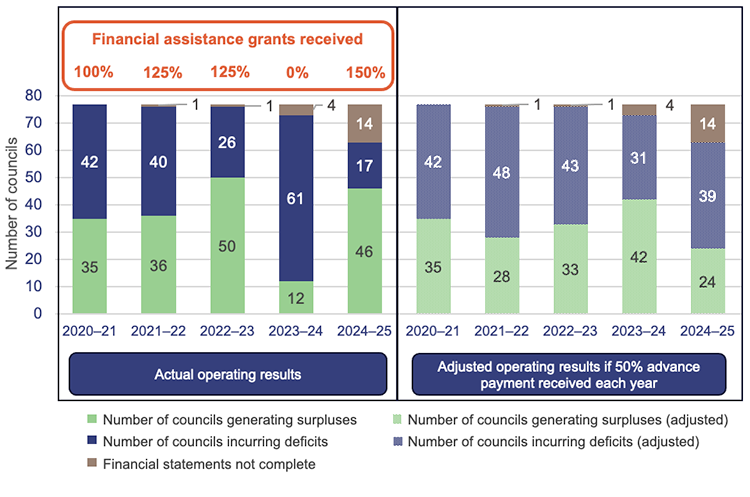

In 2024–25, the 46 councils (60 per cent of the sector) reported operating surpluses, meaning they earned more revenue than they spent on their operations. This reversed the results from the prior year where the 61 councils reported operating deficits. A key driver for the improvement in 2024–25 was the timing of the receipt of the federal financial assistance grants, which increased council revenues. The impact of the timing and the quantum of financial assistance grants on the sector’s performance is discussed further below.

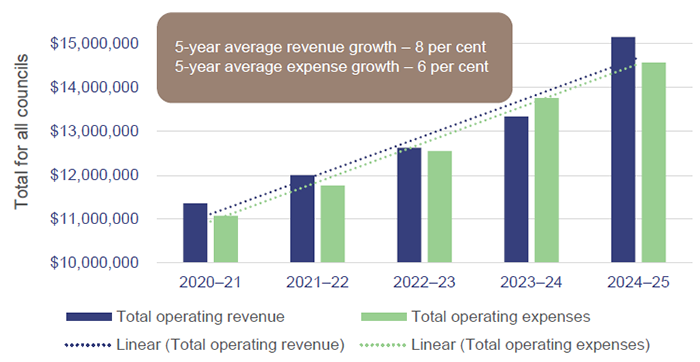

In Figure 5A, we summarise the sector’s financial performance over the last 5 financial years. It shows that the sector’s operating revenues (revenue generated from its day-to-day operations, including grants received for operational purposes from the state and Australian government) were slightly higher than the operating expenses (expenditure incurred on its day-to-day operations).

Compiled by the Queensland Audit Office, from councils’ certified financial statements available 31 October 2025.

Over the 5-year period, the sector’s yearly average operating revenue grew by 8 per cent. In the same period, the sector’s yearly average operating expenses grew by 6 per cent. This was driven by annual average increases in:

- rates, fees, and charges (primary revenue for the sector) by 6 per cent – resulting from population growth translating to higher revenue to council, combined with increases in council rates and charges determined by council through its annual budgeting process

- operating grants recognised in the financial statements (including financial assistance grants) by 27 per cent

- employee costs by 6 per cent – driven by increases in pay levels and a 2 per cent increase in the workforce

- materials and services cost by 8 per cent – resulting from higher cost of running council operations

- depreciation expense by 6 per cent – mostly driven by the increased value of council assets resulting from asset revaluations.

Results of councils’ financial sustainability measures

Several factors contribute to the sustainability outcomes for councils, including:

- increasing demands for services

- ageing infrastructure, which needs more maintenance

- rate and fee revenue, particularly in councils that are in tiers 5–8, has not kept pace with changing community needs and cost pressures.

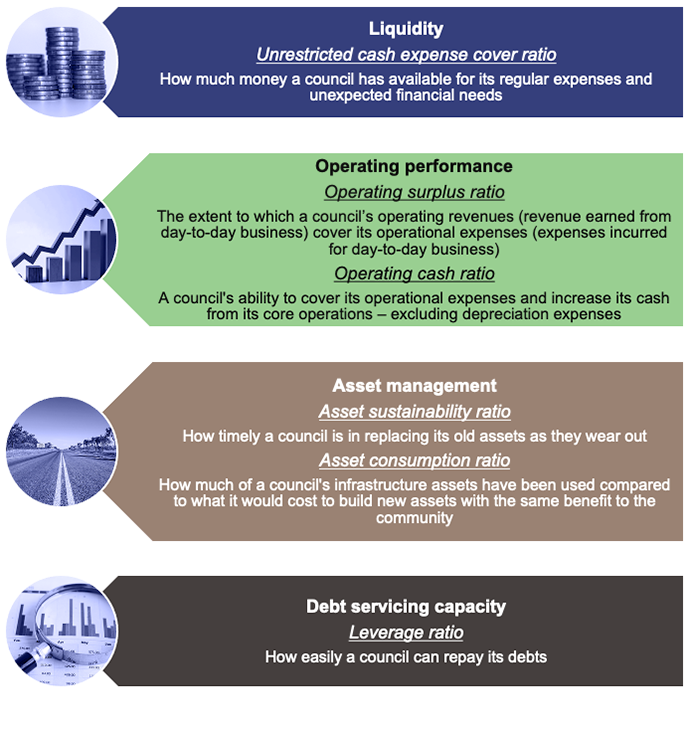

Under the department’s Financial Management (Sustainability) Guideline (2024) (the sustainability guideline) introduced in the 2023–24 financial year, councils report on various ratios to measure their financial sustainability.

The sustainability guideline assigns a benchmark for each ratio, and it varies by what tier the council is categorised into. Figure 5B provides a summary of the ratios that councils report in their financial statements.

Queensland Audit Office.

The sustainability guide recognises that performance of the sector should be assessed over the medium term and not based on council’s ability to generate operating surplus (excess of operating revenue over operating expenses) in any one year. This is because there will be certain years when councils may receive more funding or spend more than planned due to unforeseen reasons.

When councils generate operating surpluses over a medium to long term, they are well placed to be financially sustainable in the long term.

For this reason, the guide requires councils to report on the sustainability ratio using a 5-year average.

Appendix K provides a summary of the financial sustainability measures that councils must report on in their financial statements, along with guidance on how these are calculated.

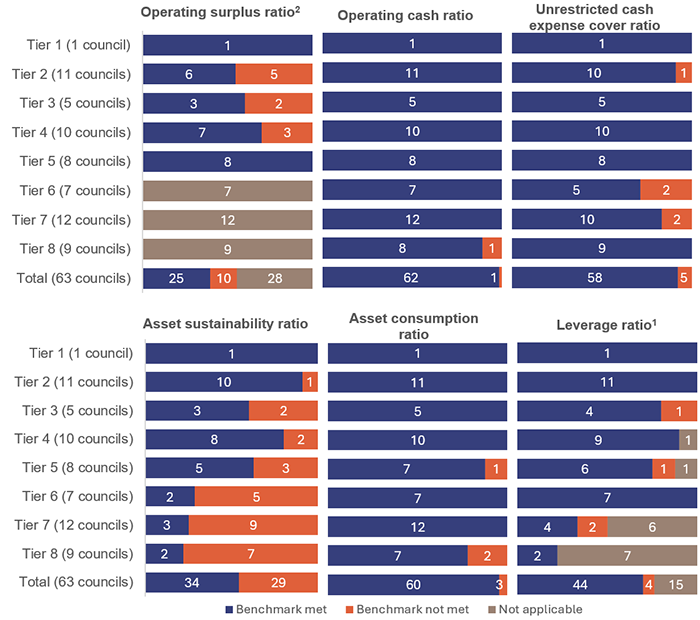

Councils in tiers 5–8 are less able to meet their asset benchmarks

Financial sustainability ratios provide meaningful information to council executives and elected members in understanding their current levels of financial sustainability and how they plan for long-term sustainability in future years.

Figure 5C shows that most councils in tiers 5–8 have not met the asset sustainability ratio. This means that these councils have not replaced their assets as they wear out. The councils typically do not have the ability to generate much in the form of own source revenue and are reliant on funding from the state or Australian Government to assist with replacing their assets.

Notes:

The above table does not include 14 councils that had not completed their financial statements by the 31 October 2025 statutory deadline.

1 Only applicable for councils that have borrowings

2 Councils in tiers 6–8 do not have a benchmark for measuring their operating surplus ratios.

* The ratios above compared to benchmark is based on 5-year average, except for the unrestricted cash expense cover ratio that is measured at 30 June 2025, as required under the department’s sustainability guideline.

Compiled by the Queensland Audit Office, from councils’ certified financial statements available 31 October 2025.

Attracting and retaining staff supports sustainability outcomes

The councils that face sustainability challenges also often have difficulties in attracting and retaining appropriately qualified staff, meaning they are reliant on consultants and contractors to deliver their day‑to-day operations.

Filling the gap by using consultants and contractors can be more expensive than employing staff and does not support the building of capability to undertake the work in the long term.

An alternate solution is to work collaboratively with other councils by sharing staff and their capabilities, for example:

| sharing technical resources or functional roles, such as accounting, financial management, information technology, project management, and governance or payroll and accounts payable functions. This could streamline processes, promote consistency and efficiency, and achieve better value for money. |

| working together on regional initiatives, including major event planning. This would enable councils to pool knowledge, avoid duplication, and deliver infrastructure and services more efficiently. |

These collaborative approaches would support more resilient operations and help councils manage financial and service delivery pressures over the long term.

We are currently undertaking a performance audit on improving sustainability in local government, in accordance with our Forward work plan 2025–28. It will focus on how the department is monitoring the long-term sustainability of councils and helping them to improve.

Variability in the timing of financial assistance grants should be adjusted in performance assessments

All local governments receive grants – known as financial assistance (FA) grants – from the Australian Government, for their day-to-day operations. These grants supplement the revenues of councils and form a substantial part of the sector’s funding.

The FA grants are provided to councils to help fund essential, day-to-day operations and capital projects. These grants are essential for councils across Australia to provide the required level of services to their community and hence considered as operating revenue for councils.

The FA grants are allocated to each council based on a determination by the Grants Commission – an independent body appointed by the Governor of Queensland.

The total amount of funding and the timing of the payment is determined by the Australian Government, and the Queensland Government distributes the grants when the payment is paid.

Under the Australian accounting standards, these grants are considered as ‘untied’ – meaning councils are free to spend them for any purpose. As such, they are recognised as revenue in the year in which they are received.

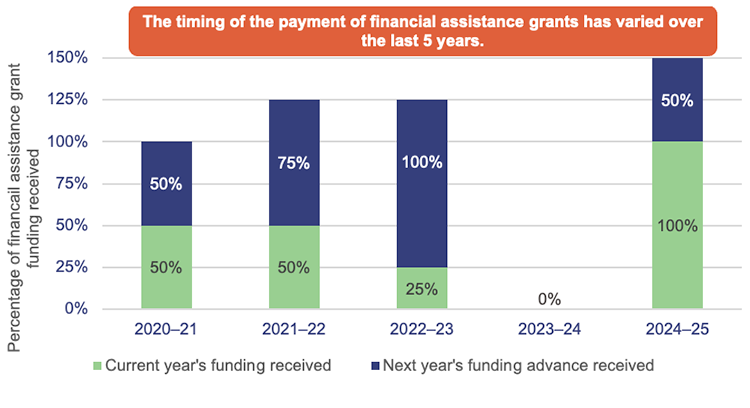

Changes in the timing of the payment of these grants have affected the sector’s performance over the past 5 years. Until 2021–22, councils typically received 50 per cent of their FA grants in advance and the remaining 50 per cent in arrears.

The payment pattern changed in 2021–22. As a result, certainty over how much funding councils receive in a given financial year has become heavily dependent on the timing of payments.

In Figure 5D, we show the per cent of FA grants received by the sector each year over the past 5 years.

Queensland Audit Office.

In the 2021−22 and 2022−23 financial years, councils received 125 per cent of their FA grants entitlement. In 2023–24, they did not receive any FA grant funding, as the full amount had already been paid in 2022–23, and no advance payment was made for 2024–25.

This year, councils received their full entitlement for 2024–25, along with an additional 50 per cent advance payment for 2025–26. This is in line with the historical practice of providing 50 per cent advance funding.

Figure 5E shows councils’ actual reported results compared to what their result would have been if they had consistently received 50 per cent of the FA grant funding in advance.

Note: Adjusted results represent councils’ operating results excluding any payment of the financial assistance grant.

Queensland Audit Office.

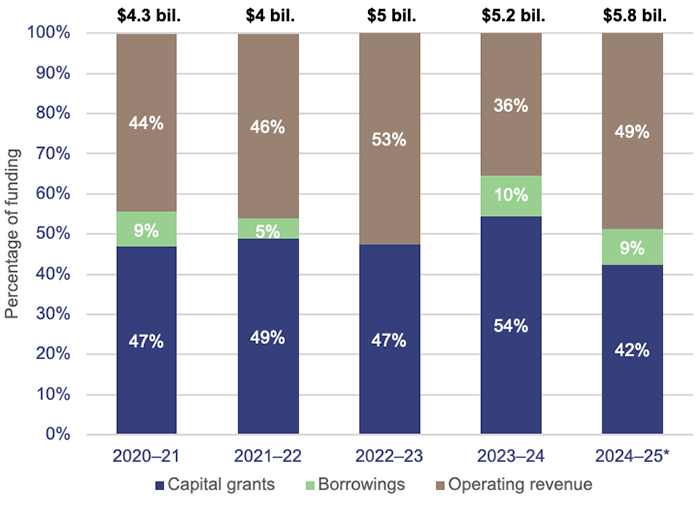

Councils spend a large proportion of their budgets on assets

In 2024–25, the sector spent $5.8 billion (2023–24: $5.2 billion) on its assets – an increase of 11 per cent from the previous year. They spend money on maintaining existing assets and building new ones for their community.

The increases in councils’ overall expenditure on assets are largely driven by increases in the costs of labour for constructing or renewing assets. When compared to the total value of community assets, councils’ spending has remained proportionate at just over 3 per cent per year for the past 3 years.

The spending is funded through grants, operating revenue, and borrowings as shown in Figure 5F.

Note: * For 2024–25, we have included the financial information of 14 councils using their last available certified financial statements, as they had not completed their 2024–25 financial statements by the 31 October statutory deadline.

Compiled by the Queensland Audit Office, from councils’ certified financial statements available as of 31 October 2025.

The asset consumption ratio is important in maintaining assets

As stated in Figure 5A, the asset consumption ratio (ACR) measures how much of an asset has been consumed/used by council. It measures the current value of a council’s assets relative to what it would cost to build new assets with the same benefit to the community.

This ratio is particularly beneficial to councils as it provides:

- an indication of how much of the asset’s life is left to be consumed

- information to determine if they are spending enough on asset renewal

- a basis for setting realistic budgets for asset maintenance and replacement

- a measure to help elected members, key decision-makers (such as chief executive officers), and the community to understand the state of critical infrastructure and the financial planning behind it.

Importance of measuring asset consumption ratio by asset classes

The department’s sustainability framework currently requires councils to measure and report the ACR as a combined ratio for all asset types. However, the ACR becomes a useful measure only if it is analysed for each asset class (for example, by road assets or water assets).

This is particularly relevant for road assets. Severe rain events or natural disasters mean road assets are often renewed using disaster recovery funding. As a result, road assets are generally maintained to a high standard and when combined with the other asset classes, they can skew a council’s overall ACR. This could potentially give a misleading picture of the condition of the council’s assets.

We identified this in Local government 2024 (Report: 13: 2024–25), when we explained that 35 councils’ water infrastructure assets had an ACR that was below the benchmark as required under the department’s sustainability framework. This year, the number of councils below the benchmark decreased to 29 councils.

|

| Opportunities for councils – monitor the asset consumption ratio (ACR) by asset class for better insights on asset condition and replacement time frames In our report, Local government 2024 (Report: 13: 2024–25), we made a recommendation to the department to consider amending the sustainability framework so councils have to measure and report the ACR for each asset. This would provide more meaningful information on the sector’s asset condition and help with good decision-making. Until the department makes this change, councils are encouraged to measure and manage their ACR at an asset class level. |